A recipe I like for long-term investment is to look for businesses that operate on high margin, produce high investment return, generate a lot of cash, and trade at attractive valuation. The recently debuted Chinese online gaming company Giant Interactive (GA) is one that I find meet all of these conditions.

GA is a three-year-old company and a new-comer to the Chinese online gaming industry, specializing in MMORPGs (Massively Multiplayer Online Role-Playing Games). Its first MMO game, ZT Online, went into commercialization only in January 2006. However, this game proved the company to be a super-runner. ZT Online was rated the most popular online game in China in the same year by both IDC and game players.

ZT Online’s great start presented itself well in the company’s financial performance. Its first six months (following commercial launch) brought in RMB 82.4M revenue and 43.5M net income. Each of the following two six-month periods recorded three-digit sequential growth. Revenue for the second six-month period (ending December 2006) increased by 296% sequentially to RMB 326.1M and net income increased by 362% sequentially to 201.1M. Then the third six-month period (ending June 2007) saw sequential revenue growth of 111% to RMB 687.5M and sequential net income growth of 155% to RMB 512.3M.

Obviously this type of growth rate is not sustainable. So Q3 began to revert to the more normal sequential growth rates. In the quarter net revenue grew by 9.5% sequentially and net income grew by 9.8% sequentially over Q2 of the year. The abrupt growth deceleration appears related to the life cycle of MOM games which tend to peak roughly 18 months following commercial launch.

The peak out of ZT Online is hardly a secret. But the abruptness of the growth deceleration has caught the street by surprise. Shares of GA plummeted by 25.4% on Nov.20, the day Q3 result was announced. The drop from previous day’s intraday high to the day’s intraday low was even more spectacular, at 41.1%.

The street’s naivete and irrational speculation can mean a great opportunity for rational investors. The challenge is of course to identify true winners. GA appears to be a clear winner by the criteria stated at the beginning of this article.

Being a high-tech service company and in the lucrative online gaming industry, the company enjoyed exceptional profit margins. For 2006, gross margin was 88.9%, operating margin 59.6%, and net margin 59.9%. For the first nine months of 2007, gross margin was 89.7%, operating margin 73.3%, and net margin 73.4%. Net income and margin were helped by the company’s current tax-exemption status (total exemption for 2006 and 2007; 50% reduction from regular tax rate of 15% as a high tech company, or 7.5%, 2008 through 2010).

Since China is implementing a new tax law, starting 2011 the company might be paying either 15% or 25% income tax (not clear yet). At the more stringent regular tax rate of 25%, NOPAT (net operating profit after tax) margin for FY 2006 and first nine months of 2007 were 44.7% and 55.0%, respectively. This means that the company would still have pocketed $0.45 and $0.55 of net profit for each dollar of sales it had made in FY 06 and first nine months of 2007, respectively, had it been taxed at the hypothetical 25% tax rate.

Seasoned investors understand that great earnings do not always translate into great cash flows. A common cash-flow problem is caused by growing accounts receivables. GA certainly does not fall into this category. Game players prepay for virtual products and services offered in its online MMO games (currently mainly ZT Online). Not only are there no accounts receivables to worry about, but also does the company collect deferred revenues (prepayment for game cards and game points) which accumulate to operating cash flow immediately.

As such, GA’s cash flow from operations actually surpasses net income. In addition, the company’s free cash flow has surpassed net earnings as well, due to relatively moderate capital expenditures.

Cash was accumulated so fast that at the end of 2006 and Q3 2007 it significantly surpassed the shareholders’ equity. Cash was so plentiful that about RMB 900M was advanced to finance CEO Mr. Shi Yuzhu’s other business (Shanghai Jiante) in Q1 and Q2. Without such cash advances, Q1 and Q2 07 would also have registered cash and equivalents that significantly surpass total shareholders’ equity. During Q&A session of the Q3 conference call, CFO Mr. Eric He boasted about having plentiful operating cash flow onshore that they can afford to leave the IPO proceeds offshore in a U.S. account for the time being.

That fast-participating cash along with no debt (who needs that with so much cash) makes invested capital (which involves taking away cash and adding debt to equity) appear virtually non-existent. In other words, the ROIC (return on invested capital) appears astronomically high, making the management seem magicians who can turn air into gold.

An alternative measure of investment return is ROE (return on equity). For the one-year period (TTM) ending September 30 2007, I have used the average of year end 2006 and Q3 2007 as an approximation of equity (out of lack of balance sheet data for Q3 06) which is RMB 616.9M. And again I have stripped off the positive impact from the company’s current tax-exemption status by using NOPAT at the hypothetical 25% tax rate, which is $664.9M. These translate into an ROE of 108% for the one-year period ending September 30 2007.

Of course, with the immense IPO cash proceeds the ROE will no longer remain at this level. My estimate for FY 07’s ROE, using average equity for the year and NOPAT at the hypothetical 25% tax rate, is about 23%. The corresponding estimate using FY 07’s net profit (derived from the company’s low revenue projection for Q4) is about 31%. Again note these are the returns when the entire equity is virtually cash. Presently the company has about RMB 6.8B of cash (including both cash generated from operation and the IPO proceeds).

Technically speaking ROE is not as insightful a measure as ROIC. But in GA’s case where ROIC is ridiculously high ROE gives us an alternative way to see the exceptional return the company generated while still virtually hoarding all its equity as cash in the bank. As such, the company is simply in a great position to expand its business and withstand any downturn.

GA's solid cash position also means that, in the intermediate term, it will not have to pursue additional financing (like issuing bonds, secondary public offering, etc.) that could have a negative impact on the share price.

To value this company, I used a DCF model with 16% discount rate. Here are the assumptions I made: (1) the company will be in business for the next 30 years only, (2) free cash flow (FCF) is equal to net earnings, (3) the company will grow FCF or earnings at 27% annual rate for the first five years (starting 08), followed by 15% for the next five years and 7% for the remaining 20 years. I arrived at $12.30 (per share) when I used the hypothetical (25% tax rate) NOPAT for this year, and $16.32 (per share) when I used an estimated net earnings for FY 07. So this model puts the stock at $12.30 to $16.32 per share.

It should be obvious that this model used largely conservative estimates. Particularly, the 16% discount rate used was quite stringent. Moreover, the initial growth rate was assumed to be below some analyst’s forecast of 30 to 40% revenue growth rate for the Chinese online gaming industry as a whole in the next few years. According to iResarch, the industrial revenue in 2006 grew 60% over 2005. And it reached RMB 3.04B in Q3 2007 alone, compared to RMB 7.68B for whole year 2006. As of Q3 GA's market share was third in the industry, at 13.8%, only trailing NetEase's 15.1% and Shanda's 18.4%.

If you have not followed this company, you could be wondering where the growth comes from given ZT Online has likely peaked. The answer is GA certainly is not a one-trick pony. The company's second online game, Giant Online (a 2.5D MMO game) is in closed beta testing and has already attracted thousands of players. Based on data collected from the beta testing, Mr. Shi expects this game to generate at least the same level of revenue as ZT Onlne. Furthermore, the company will be rolling out its licensed 3D game King of Kings III next year. And you can count on more games to be developed and released in the future.

Investing in GA is more or less capitalizing on CEO Mr. Shi Yuzhu’s past success and failure. Mr. Shi is a high-profile entrepreneur in China. As early as 1993, his software company Zhuhai Giant Group was the second largest private enterprise in China. In 1995 he was ranked 8th on Forbe’s first-ever China rich list. In the mid 1990s, Zhuhai Giant even received the attention and visits from China’s top leaders like Li Peng (former Premier), Hu Jintao (current President), and Zhu Rongji (former Premier). Mr. Li Peng (then Premier) was reported to have visited Zhuhai Giant once a year during that period.

Unfortunately, Mr. Shi’s enterprise collapsed around 1997 due to over-ambitious business expansion, real estates speculation, and disregard of fundamental business principles. Mr. Shi’s fall became one of the most famous in China’s modern enterprise history.

But Mr. Shi proved that he can learn and benefit from failure, even a major one. In early 2000s Mr. Shi reemerged with great strength through successful healthcare and nutrition businesses (Shanghai Jiante, etc.) and equity investment (Giant Investment, etc.). That enabled him to venture into the lucrative online gaming industry in late 2004. In just a year, his first MMO product ZT Online hit the market with great success.

Other than Mr. Shi’s well known marketing acumen, it appears there are two other key elements that have helped Mr. Shi to reemerge and will empower him for a lasting success. One element Mr. Shi learned from his Zhuhai Giant collapse, i.e., cash position and liquidity is the life of enterprise. The other element he discovered in his previous success and it is called high margin businesses. Mr. Shi does not believe in low-margin high-volume businesses. He thinks the way to business success is to focus on high-margin areas.

And so far we have seen GA’s enormous cash-generating power and high profit margins to be well aligned with Mr. Shi’s philosophy.

Mr. Shi understands the online gaming industry by being a regular game player himself. Even before he founded Shanghai Zhengtu, he had acquired unique insight into virtual products, absentee role-experience-level boost, external game-cheating programs, etc. Some credited him with being the first to introduce the free-to-play business model into China, even though Shanda was officially the first to announce it. It was said that one of Zhengtu's vice presidents had accidentally let out Mr. Shi's idea to Shanda. Mr. Shi's gaming industry insight will continue to be a key contributor to GA's success.

Mr. Shi is also a close friend of China's business heavy-weights like Mr. Duan Youngji (Co-founder, CEO and Chairman of Stone Group) and Liu Chuanzhi (Co-founder, former CEO and Chairman of Lenovo). Mr. Duan and Liu were Mr. Shi's coaches even during his most difficult times.

Most of GA’s current senior management (President Liu Wei, COO Zhang Lu, and vice presidents) has at least worked with Mr. Shi either since Zhuhai Giant or Shanghai Jiante. Mr. Shi thinks the great fall that he and his team have been through together is his most precious asset. Along with the lessons learned from the previous notorious failure, this loyal management team has full knowledge and thorough understanding of Mr. Shi’s unique marketing methodology and operational philosophy.

GA’s CFO Mr. Eric He is a Wharton School MBA and CPA and Chartered Financial Analyst in the U.S. He has quite extensive financial career background. It is clear from Q3 conference call that Mr. He stands out among the CFOs of young Chinese companies in terms of communication with U.S. analysts.

Enough good has been said about this company. Now I do want to throw in a few chilling words of caution.

Firstly, the lucrative online gaming industry is also where the best young Chinese entrepreneurs are. Mr. Shi is competing with the likes of Mr. Ding Lei (NetEase) and Mr. Chen Tianqiao (Shanda). GA still has a great catch-up to do to capture the top spot. We have seen a great start. But whether Mr. Shi and his team can keep the momentum going remains to be seen. If Mr. Chen Tianqiao is right, however, the online gaming industry is growing fast and has room for multiple players to coexist and grow together.

Secondly, the insiders have too much power by owning the majority stake of the company. Following the IPO, the senior officers own 57.22% of the company. Forgive me for not mentioning the benefit of insider ownership.

Thirdly, the prepayment business gives the management a lot of room to manipulate the deferred revenues. Quarters can be easily made stronger or weaker than they actually are. For example, given the precipitous drop in sequential growth in Q3, could Q1 and Q2 have been dressed up at the expense of Q3 and Q4 to boost IPO performance?

No, I’m not suggesting they have done that. It is my hope the management has not taken and will never take advantage of the deferred revenues to dress up or down quarterly or annual financial performance. A truly smart management will never do that. After all, they are supposed to follow GAAP. But if they are truly brilliant, they should have learned from the recent class action lawsuits filed against them.

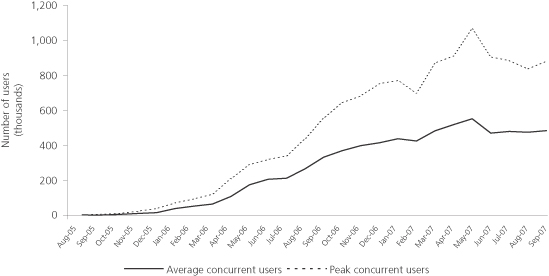

GA's prospectus disclosed (p.1) PCU and ACU of 888,146 and 481,054, respectively, for Q3 2007. It also included a chart (p.94, click here to view) that plots monthly ACU and PCU versus time through September 07. PCU and ACU decline can be seen starting in June and lasting into Q3. The prospectus also attributed the decline to game rule changes. Still, it has not prevented law firms from alleging failure of disclosure on declining ACU and PCU in Q3.

The management should understand that cash-rich companies make perfect target for class action suits. So it has no choice other than remaining fully honest and transparent when it comes to financial disclosure. After all, it is quite dramatic for a company to be in class action suits less than a month after going public.

Disclosure: the author owns GA as of this writing. This post represents only the author's personal opinion. It should not be interpreted as a recommendation to buy or sell GA stock.

Friday, November 30, 2007

Wednesday, November 07, 2007

Wall Street's No Confidence Vote on TCM’s Management

The market is a voting machine in the short run and a weighing machine in the long run. That was how Benjamin Graham, the Father of modern security analysis, characterized it. Today, shareholders of Tongjitang Chinese Medicines (TCM) overwhelmingly voted “no confidence” on TCM’s management team. Shares of TCM closed down 25.87% on heavy volume.

Before the market opened CIBC World Markets analyst Elliot Wilbur downgraded Tongjitang to "Sector Perform" from "Sector Outperform”, citing disappointing revenue growth from the company’s flagship product XLGB (Xianling Gubao). Following her lead, investors run for exit in great panic, in a day when S&P 500 lost 2.94% and FXI lost 4.77%.

In the third quarter XLGB sales grew only a paltry 2% year over year. The management attributed the slow growth to a combination of three factors. First, TCM obtained the national trade secret status for XLGB which provided for manufacturing exclusivity and pricing protection. As a result, the company was ready to raise its selling price and accordingly scaled back sales and marketing effort. Second, unusually warm weather in certain regions has served to reduce its sales since warmer temperature tends to lessen symptom of osteoporosis, particularly among senior patients. Third, flooding in certain areas served to reduce the number of trips patients made to hospitals and retail pharmacies.

Apparently shareholders did not want to listen to excuses. But is this (paltry XLGB growth) the sole factor behind CIBC’s downgrade and investors’ panic exodus? It does not appear so simple to me. The 26% single-day drop is essentially a loud “no confidence” vote on TCM’s management. And it is not all about XLGB.

If you are like me, what appears the most worrisome is actually the management’s asset management strategy. Since Q2 (although I just found out from Q3 conference call) the company has invested a fraction of its cash reserve in Chinese IPOs listed in Hong Kong or mainland exchanges. In Q3, TCM recorded a RMB 4M gain from these short-term investments. As of end of Q3, the company has RMB 41.4M (about 5.1% of company’s total cash reserve) invested in these junior Chinese securities.

In the Q&A session of the Q3 conference call, management revealed the IPO investment program will continue through at least the end of Q4. Whether they will continue this program into 2008 depends on cash reserve available and market condition ("extent of market activity," to use the management's original words) then. The management intends to allocate 10-15% of cash for investment in Chinese IPOs.

Moreover, the company’s IPO proceeds were still mostly deposited in US$. Management explained that this was due to the stringent foreign currency regulation in China that limits conversion into RMB. It also partly justified its IPO investment program as a way to hedge the loss incurred by the depreciation of US$ against RMB.

From management’s remarks, it appears the IPO investments are mostly short-term oriented. There was no mentioning of valuation considerations, only market condition. It seems the hotter the market is, the more likely the company is going to stay in this game. Given today’s frothy Chinese stock market, it makes me wonder if the management’s vocabulary contains the word “risk” at all.

Secondary to the cash management, analysts were concerned about the rise of accounts receivables (A/R). Based on my calculation, A/R turnover increased to about 131 days at end of Q3 compared to 118.5 days as of end of 2006. Management indicated they are aware of this problem and is working to improve it significantly in Q4. Let’s follow up on how well they keep their words three months later.

Obviously, these are more than enough for investors to scream “enough is enough.”

I also noted a significant increase in inventories. Inventories turnover increased to about 134 days from 78.5 days as of end of 2006. I do not know if this inventories build up was on finished goods or on raw materials (I intended to ask about this during the conference call; but operator cut me off). If it was due to stock-up of barrenwort or other raw materials this would be a non-issue, since it could be a great strategy to lock down raw materials cost in an inflationary environment. The price of barrenwort has skyrocketed in the past couple of years until recently.

Then, wasn’t there anything encouraging out of the quarter? Sure yes.

Sales of other core products excluding XLGB (Moisturizing and anti-itching capsules, Zaoren Anshen capsules, and Daibaizhu Syrup) increased 723% to RMB 25.5M. The company’s OTC strategy seems to have worked pretty well, particularly the Moisturizing and anti-itching capsules which have registered more sales to the OTC market (retail pharmacies) than to the prescription market (hospitals). To understand why OTC strategy is important, please read my previous post.

And although Q3 is the seasonally weakest quarter, it also has grown significantly faster than the other quarters so far this year. Net revenue has grown 28.7% YoY in the quarter compared to growth YoY of 24.9% for the first nine months of the year. Gross profit has grown 34.1% in the quarter compared to growth of 22.5% for the first nine months. Operating income has grown 147.1% in the quarter vs. growth of 15.6% for the first nine months. Net income has grown 464.7% in the quarter vs. 52% for the first nine months. Net income in the quarter was greatly helped (and skewed) by interest income (mainly from the IPO proceeds), investment gain, government grant and a gain associated with disposal of Guizhou LLF’s liabilities. Acquisition of Guizhou LLF is expected to complete by the end of year. LLF will contribute an estimated RMB 10M of revenue in Q4.

By my calculation, ROE and ROC for the past twelve months were roughly 23.7% and 19.8%, respectively. Admittedly these numbers were helped by the tax exemption status, and also slightly by the unusual gains mentioned above. But they were also diluted by a greatly expanded equity and capital base associated with the huge and non-productive cash reserve generated from the IPO earlier this year.

Another encouraging piece of news is that the company has obtained a legal “nationally well-known brand” for its Tongjitang name. This marked an important victory for the company in its brand protection endeavors. It allows the company to weigh its legal options against Hubei Tongjitang, Sanjin Group’s Tongjitang subsidiaries, and any other company that attempts to steal the Tongjitang brand. You can read more about this in this post. As a follow up and clarification to that post, company CEO Mr. Wu Xiaochun is a major shareholder in Shanghai Tongjitang and use of the word Tongjitang there was by an agreement with Guizhou Tongjitang, TCM’s major operating company.

On top of these, you can also add the 11 potential new products on company's pipeline, encouraging clinical result from Synarc, and the active acquisition efforts being undertaken. Not counting Guizhou LLF, the company's current products include 15 modernized traditional Chinese medicines, 38 western medicines, and 4 nutritional products.

Coming back to XLGB, management expects its normalized growth rate to be in the vicinity of 20%. On a TTM basis, XLGB has generated a net revenue of RMB 437.3M as of end of Q3, compared to RMB 374.6M for FY 2006. This means that if XLGB proves to bring in zero growth in Q4, we will be looking at 16.7% growth for XLGB in FY 07. For XLGB sales to reach the 20% ball mark in FY 07, Q4 growth on XLGB has to be about 9.5%. This looks an achievable target for Q4.

In fact if you assume XLGB grows 20% and non-XLGB products grow 40.8% in FY 07, you would arrive at RMB 605M total revenue for the year. And this is precisely the midpoint of the managment's projection (RMB 590-620M) for the year. What's to be ashamed of these growth numbers (20% flagship product and double that rate for other products)?

To the management, XLGB’s long-term potential can be seen from its room to grow in China. At this stage, XLGB is only carried in 2400+ out of more than 20,000 hospitals and 34,000+ out of 250,000 retail pharmacies.

All in all, management’s execution does not look all that bad so far this year. Management has demonstrated ability to execute in OTC market, product diversification (non-XLGB and new products), brand protection, acquisition initiatives, and more. (Investors might like to see a faster pace of acquisition than is already achieved though.) Long-term investors will look beyond the quarter and the year to get at the whole picture. They will not be part of the voting machine.

However, I’m very concerned about management’s cash management strategy going forward. The Wall Street has voted out loud in protest against the management’s reckless way of asset management. This is a critical test on the management’s willingness to listen to shareholder voices, sincerity in enhancing shareholder value, and overall wisdom and intelligence. Unless the company has a long-term plan to Chinese equity investment and imparts adequate valuation considerations, the obvious smart choice is to stop this reckless practice before it is too late. Meanwhile I urge my fellow investors to open dialog with the management to find out more about this.

How the market will weigh TCM in the long run rests on the management completely.

Disclosure: the author owns TCM as of this writing. This post represents only the author's personal view which can be biased or incorrect. It should not be interpreted as a recommendation to buy or sell TCM stock.

Before the market opened CIBC World Markets analyst Elliot Wilbur downgraded Tongjitang to "Sector Perform" from "Sector Outperform”, citing disappointing revenue growth from the company’s flagship product XLGB (Xianling Gubao). Following her lead, investors run for exit in great panic, in a day when S&P 500 lost 2.94% and FXI lost 4.77%.

In the third quarter XLGB sales grew only a paltry 2% year over year. The management attributed the slow growth to a combination of three factors. First, TCM obtained the national trade secret status for XLGB which provided for manufacturing exclusivity and pricing protection. As a result, the company was ready to raise its selling price and accordingly scaled back sales and marketing effort. Second, unusually warm weather in certain regions has served to reduce its sales since warmer temperature tends to lessen symptom of osteoporosis, particularly among senior patients. Third, flooding in certain areas served to reduce the number of trips patients made to hospitals and retail pharmacies.

Apparently shareholders did not want to listen to excuses. But is this (paltry XLGB growth) the sole factor behind CIBC’s downgrade and investors’ panic exodus? It does not appear so simple to me. The 26% single-day drop is essentially a loud “no confidence” vote on TCM’s management. And it is not all about XLGB.

If you are like me, what appears the most worrisome is actually the management’s asset management strategy. Since Q2 (although I just found out from Q3 conference call) the company has invested a fraction of its cash reserve in Chinese IPOs listed in Hong Kong or mainland exchanges. In Q3, TCM recorded a RMB 4M gain from these short-term investments. As of end of Q3, the company has RMB 41.4M (about 5.1% of company’s total cash reserve) invested in these junior Chinese securities.

In the Q&A session of the Q3 conference call, management revealed the IPO investment program will continue through at least the end of Q4. Whether they will continue this program into 2008 depends on cash reserve available and market condition ("extent of market activity," to use the management's original words) then. The management intends to allocate 10-15% of cash for investment in Chinese IPOs.

Moreover, the company’s IPO proceeds were still mostly deposited in US$. Management explained that this was due to the stringent foreign currency regulation in China that limits conversion into RMB. It also partly justified its IPO investment program as a way to hedge the loss incurred by the depreciation of US$ against RMB.

From management’s remarks, it appears the IPO investments are mostly short-term oriented. There was no mentioning of valuation considerations, only market condition. It seems the hotter the market is, the more likely the company is going to stay in this game. Given today’s frothy Chinese stock market, it makes me wonder if the management’s vocabulary contains the word “risk” at all.

Secondary to the cash management, analysts were concerned about the rise of accounts receivables (A/R). Based on my calculation, A/R turnover increased to about 131 days at end of Q3 compared to 118.5 days as of end of 2006. Management indicated they are aware of this problem and is working to improve it significantly in Q4. Let’s follow up on how well they keep their words three months later.

Obviously, these are more than enough for investors to scream “enough is enough.”

I also noted a significant increase in inventories. Inventories turnover increased to about 134 days from 78.5 days as of end of 2006. I do not know if this inventories build up was on finished goods or on raw materials (I intended to ask about this during the conference call; but operator cut me off). If it was due to stock-up of barrenwort or other raw materials this would be a non-issue, since it could be a great strategy to lock down raw materials cost in an inflationary environment. The price of barrenwort has skyrocketed in the past couple of years until recently.

Then, wasn’t there anything encouraging out of the quarter? Sure yes.

Sales of other core products excluding XLGB (Moisturizing and anti-itching capsules, Zaoren Anshen capsules, and Daibaizhu Syrup) increased 723% to RMB 25.5M. The company’s OTC strategy seems to have worked pretty well, particularly the Moisturizing and anti-itching capsules which have registered more sales to the OTC market (retail pharmacies) than to the prescription market (hospitals). To understand why OTC strategy is important, please read my previous post.

And although Q3 is the seasonally weakest quarter, it also has grown significantly faster than the other quarters so far this year. Net revenue has grown 28.7% YoY in the quarter compared to growth YoY of 24.9% for the first nine months of the year. Gross profit has grown 34.1% in the quarter compared to growth of 22.5% for the first nine months. Operating income has grown 147.1% in the quarter vs. growth of 15.6% for the first nine months. Net income has grown 464.7% in the quarter vs. 52% for the first nine months. Net income in the quarter was greatly helped (and skewed) by interest income (mainly from the IPO proceeds), investment gain, government grant and a gain associated with disposal of Guizhou LLF’s liabilities. Acquisition of Guizhou LLF is expected to complete by the end of year. LLF will contribute an estimated RMB 10M of revenue in Q4.

By my calculation, ROE and ROC for the past twelve months were roughly 23.7% and 19.8%, respectively. Admittedly these numbers were helped by the tax exemption status, and also slightly by the unusual gains mentioned above. But they were also diluted by a greatly expanded equity and capital base associated with the huge and non-productive cash reserve generated from the IPO earlier this year.

Another encouraging piece of news is that the company has obtained a legal “nationally well-known brand” for its Tongjitang name. This marked an important victory for the company in its brand protection endeavors. It allows the company to weigh its legal options against Hubei Tongjitang, Sanjin Group’s Tongjitang subsidiaries, and any other company that attempts to steal the Tongjitang brand. You can read more about this in this post. As a follow up and clarification to that post, company CEO Mr. Wu Xiaochun is a major shareholder in Shanghai Tongjitang and use of the word Tongjitang there was by an agreement with Guizhou Tongjitang, TCM’s major operating company.

On top of these, you can also add the 11 potential new products on company's pipeline, encouraging clinical result from Synarc, and the active acquisition efforts being undertaken. Not counting Guizhou LLF, the company's current products include 15 modernized traditional Chinese medicines, 38 western medicines, and 4 nutritional products.

Coming back to XLGB, management expects its normalized growth rate to be in the vicinity of 20%. On a TTM basis, XLGB has generated a net revenue of RMB 437.3M as of end of Q3, compared to RMB 374.6M for FY 2006. This means that if XLGB proves to bring in zero growth in Q4, we will be looking at 16.7% growth for XLGB in FY 07. For XLGB sales to reach the 20% ball mark in FY 07, Q4 growth on XLGB has to be about 9.5%. This looks an achievable target for Q4.

In fact if you assume XLGB grows 20% and non-XLGB products grow 40.8% in FY 07, you would arrive at RMB 605M total revenue for the year. And this is precisely the midpoint of the managment's projection (RMB 590-620M) for the year. What's to be ashamed of these growth numbers (20% flagship product and double that rate for other products)?

To the management, XLGB’s long-term potential can be seen from its room to grow in China. At this stage, XLGB is only carried in 2400+ out of more than 20,000 hospitals and 34,000+ out of 250,000 retail pharmacies.

All in all, management’s execution does not look all that bad so far this year. Management has demonstrated ability to execute in OTC market, product diversification (non-XLGB and new products), brand protection, acquisition initiatives, and more. (Investors might like to see a faster pace of acquisition than is already achieved though.) Long-term investors will look beyond the quarter and the year to get at the whole picture. They will not be part of the voting machine.

However, I’m very concerned about management’s cash management strategy going forward. The Wall Street has voted out loud in protest against the management’s reckless way of asset management. This is a critical test on the management’s willingness to listen to shareholder voices, sincerity in enhancing shareholder value, and overall wisdom and intelligence. Unless the company has a long-term plan to Chinese equity investment and imparts adequate valuation considerations, the obvious smart choice is to stop this reckless practice before it is too late. Meanwhile I urge my fellow investors to open dialog with the management to find out more about this.

How the market will weigh TCM in the long run rests on the management completely.

Disclosure: the author owns TCM as of this writing. This post represents only the author's personal view which can be biased or incorrect. It should not be interpreted as a recommendation to buy or sell TCM stock.

Thursday, November 01, 2007

Brand Protection Key to TCM’s Long-Term Success

My kind reader Rick posted a comment on my blog asking for one or two negatives on Tongjitang Chinese Medicines (TCM). In response I have posted a few risks associated with investing in this stock. For most part, they are either uncertainties in the Chinese pharma industry or minor issues common to small caps. But I do want to single out the brand protection issue and discuss it a little more here.

Although not as famous as Tongrentang (which dates back to 1669 and is probably the best-known “senior” medical brand in China), Tongjitang is still a well respected brand in China. The brand dates back to 1888 when once-governor of Yungui (Yunnan and Guizhou provinces) Mr. Tang Jiong and his friend invested 2000-liang (2025 ounces) of silver to open Tongjitang Drugstore.

Gradually Tongjitang was renowned for its highly proficient physicians, quality drugs, genuine ingredients, fair pricing, and business ethics. The reputation even spread overseas. So there was a legend about an overseas Chinese (in serious illness) traveling from Southeast Asia to Guiyang to seek medical treatment from Tonjitang around 1940. There he recovered from his illness in just one month. To express his gratitude he offered to pay a huge sum to Tongjitang. But the drugstore firmly declined his offer based on its business principle. This legend was said to have made the brand famous in various regions of the country.

Like many other senior brands, in the past half-century or so Tongjitang has gone through chaotic times. But the brand managed to survive and was revigorated following the buy-out by Mr. Wang Xiaochun’s Guizhou Xianling. TCM’s heavy advertising and marketing spending in recent years has helped to strengthen the brand.

Naturally what come with a great brand are not just praises and flowers. There also come infringement and plagiarizers. In the Chinese market, not only are there counterfeit XLGB medicines there are also related and unrelated medicines sold on plagiarized Tongjitang brand. In the past, the company has worked with several provinces to crack down counterfeit XLGB products with some success. But by briefly browsing the customer questions section of Guizhou Tongjitang Pharmaceutical’s (TCM’s major operating company) web site, there still appears to be some customer concerns regarding counterfeit XLGB products. Furthermore, in the service complaints as well as the customer questions sections there were two or three reports of skin-related medicines sold on counterfeit Tongjitang brand.

Several enterprises have also competed to take a share of the Tongjitang brand. I have knowledge of three companies (other than TCM) that use the word “Tongjitang” in their company names. They are Shanghai Tongjitang, Hubei Tongjitang, and Sanjin Pharma’s Tongjitang subsidiary. All these companies seem to have been endorsed by their respective local governments. Their Tongjitang brands have all been claimed to date back to the 1888-founded Guiyang Tongjitang. Yet none of them has provided a convincing story of how it is related to Guizhou Tongjitang.

The most striking example would be Shanghai Tongjitang. It owns the www.tongjitang.net domain and was founded only in August 2002. Without explaining how it is related to the genuine brand, it mysteriously boasts about Tongjitang’s more than century-old history on its web site. Now you have seen the enterprise version of a five-year-old kid bragging about having five or six generations of descendants. Unless it is a subsidiary of Guizhou Tongjitang (which I do not believe so), this is brand infringement at its most blatant extreme. Shanghai Tongjitang claimed it was GMP certified in March 2005.

TCM management is aware of the existence of Hubei Tongjitang and Sanjin’s Tongjitang subsidiary (but I do not know if it is aware of Shanghai Tongjitang). Due to China’s inadequate regulatory and legal system, TCM will be fighting an uphill battle with these infringers. The company thinks it might need to live with these companies in the end. A thorny issue is that Tongjitang is not actually legalized as a well-known trademark in China. But I believe it would be a big mistake for the company to leave at that.

After all, Tongjitang was recognized as a “National Senior Brand” in 1994 by the then Ministry of Domestic Trade. And partly based on this recognition, the company has won a lawsuit in July on a domain-name infringement case in Changsha City, Hunan Province, according to a Guizhou Daily report. Another key point mentioned in the report was the company’s winning history in legal battles related to its Tongjitang brand. (Oh sure, this is a proof that the company has not really sat still when it comes to brand protection. Good news for shareholders.)

In my humble opinion, the company should have dedicated personnel working just to protect its brand. The top priority for this team should be to earn a legalized “well-known trademark,” using as basis its 1994 “National Senior Brand” recognition, its “Guizhou Province Well-Known Brand” recognition, and the history of legal judgments in favor of the company. Depending on the outcome of this legal battle, the company should confront the infringing businesses mentioned above and resort to legal means when necessary. Understandably, due to the various local stakes involved and China’s inadequate legal system, this legal battle is most likely a much tougher one than the domain-name case where the defendant was only an individual.

Meanwhile the company should immediately work to differentiate its Tongjitang brand from the plagiarized brands (if it has not started doing so yet). It should clearly state that Guizhou Tongjitang is the only genuine Tongjitang brand, in its various advertisements, marketing campaigns, seminars and other consumer education initiatives. Those plagiarized Tongjitang brands should also be clearly named and stated to be unrelated to the genuine “National Senior Brand.”

In the event the company cannot legalize Tongjitang as a national "well-known trademark", it should think about the possibility to acquire these infringers. Collectively (with the infringers) they should work together to guarantee the quality of their products and use a single “Tongjitang” brand. In alliance they would be powerful enough to secure a legal “well-known trademark” in China, thus preventing new comers from stealing the brand again. If this is infeasible or does not work out, the only solution would be to strengthen the brand differentiation effort described above. And that is why brand differentiation is important from the very beginning.

Successful brand protection will contribute to TCM’s long-term success, in a big way. And management’s skill, commitment, wisdom and creativity will be put to test in its brand-protection endeavor.

Disclosure: the author owns TCM as of this writing. This post represents only the author's personal view which can be biased or incorrect. It should not be interpreted as a recommendation to buy or sell TCM stock.

Although not as famous as Tongrentang (which dates back to 1669 and is probably the best-known “senior” medical brand in China), Tongjitang is still a well respected brand in China. The brand dates back to 1888 when once-governor of Yungui (Yunnan and Guizhou provinces) Mr. Tang Jiong and his friend invested 2000-liang (2025 ounces) of silver to open Tongjitang Drugstore.

Gradually Tongjitang was renowned for its highly proficient physicians, quality drugs, genuine ingredients, fair pricing, and business ethics. The reputation even spread overseas. So there was a legend about an overseas Chinese (in serious illness) traveling from Southeast Asia to Guiyang to seek medical treatment from Tonjitang around 1940. There he recovered from his illness in just one month. To express his gratitude he offered to pay a huge sum to Tongjitang. But the drugstore firmly declined his offer based on its business principle. This legend was said to have made the brand famous in various regions of the country.

Like many other senior brands, in the past half-century or so Tongjitang has gone through chaotic times. But the brand managed to survive and was revigorated following the buy-out by Mr. Wang Xiaochun’s Guizhou Xianling. TCM’s heavy advertising and marketing spending in recent years has helped to strengthen the brand.

Naturally what come with a great brand are not just praises and flowers. There also come infringement and plagiarizers. In the Chinese market, not only are there counterfeit XLGB medicines there are also related and unrelated medicines sold on plagiarized Tongjitang brand. In the past, the company has worked with several provinces to crack down counterfeit XLGB products with some success. But by briefly browsing the customer questions section of Guizhou Tongjitang Pharmaceutical’s (TCM’s major operating company) web site, there still appears to be some customer concerns regarding counterfeit XLGB products. Furthermore, in the service complaints as well as the customer questions sections there were two or three reports of skin-related medicines sold on counterfeit Tongjitang brand.

Several enterprises have also competed to take a share of the Tongjitang brand. I have knowledge of three companies (other than TCM) that use the word “Tongjitang” in their company names. They are Shanghai Tongjitang, Hubei Tongjitang, and Sanjin Pharma’s Tongjitang subsidiary. All these companies seem to have been endorsed by their respective local governments. Their Tongjitang brands have all been claimed to date back to the 1888-founded Guiyang Tongjitang. Yet none of them has provided a convincing story of how it is related to Guizhou Tongjitang.

The most striking example would be Shanghai Tongjitang. It owns the www.tongjitang.net domain and was founded only in August 2002. Without explaining how it is related to the genuine brand, it mysteriously boasts about Tongjitang’s more than century-old history on its web site. Now you have seen the enterprise version of a five-year-old kid bragging about having five or six generations of descendants. Unless it is a subsidiary of Guizhou Tongjitang (which I do not believe so), this is brand infringement at its most blatant extreme. Shanghai Tongjitang claimed it was GMP certified in March 2005.

TCM management is aware of the existence of Hubei Tongjitang and Sanjin’s Tongjitang subsidiary (but I do not know if it is aware of Shanghai Tongjitang). Due to China’s inadequate regulatory and legal system, TCM will be fighting an uphill battle with these infringers. The company thinks it might need to live with these companies in the end. A thorny issue is that Tongjitang is not actually legalized as a well-known trademark in China. But I believe it would be a big mistake for the company to leave at that.

After all, Tongjitang was recognized as a “National Senior Brand” in 1994 by the then Ministry of Domestic Trade. And partly based on this recognition, the company has won a lawsuit in July on a domain-name infringement case in Changsha City, Hunan Province, according to a Guizhou Daily report. Another key point mentioned in the report was the company’s winning history in legal battles related to its Tongjitang brand. (Oh sure, this is a proof that the company has not really sat still when it comes to brand protection. Good news for shareholders.)

In my humble opinion, the company should have dedicated personnel working just to protect its brand. The top priority for this team should be to earn a legalized “well-known trademark,” using as basis its 1994 “National Senior Brand” recognition, its “Guizhou Province Well-Known Brand” recognition, and the history of legal judgments in favor of the company. Depending on the outcome of this legal battle, the company should confront the infringing businesses mentioned above and resort to legal means when necessary. Understandably, due to the various local stakes involved and China’s inadequate legal system, this legal battle is most likely a much tougher one than the domain-name case where the defendant was only an individual.

Meanwhile the company should immediately work to differentiate its Tongjitang brand from the plagiarized brands (if it has not started doing so yet). It should clearly state that Guizhou Tongjitang is the only genuine Tongjitang brand, in its various advertisements, marketing campaigns, seminars and other consumer education initiatives. Those plagiarized Tongjitang brands should also be clearly named and stated to be unrelated to the genuine “National Senior Brand.”

In the event the company cannot legalize Tongjitang as a national "well-known trademark", it should think about the possibility to acquire these infringers. Collectively (with the infringers) they should work together to guarantee the quality of their products and use a single “Tongjitang” brand. In alliance they would be powerful enough to secure a legal “well-known trademark” in China, thus preventing new comers from stealing the brand again. If this is infeasible or does not work out, the only solution would be to strengthen the brand differentiation effort described above. And that is why brand differentiation is important from the very beginning.

Successful brand protection will contribute to TCM’s long-term success, in a big way. And management’s skill, commitment, wisdom and creativity will be put to test in its brand-protection endeavor.

Disclosure: the author owns TCM as of this writing. This post represents only the author's personal view which can be biased or incorrect. It should not be interpreted as a recommendation to buy or sell TCM stock.

Subscribe to:

Posts (Atom)

{kind=link}